Jet Fuel is Taking Flight 🛫

Jet Fuel is Taking Flight 🛫

All you need to know about the global fuel's current state of play and what to expect flying forward.

7 min read

Jet Fuel: Where are we today?

Jet fuel prices are expected to average $98.5 – $112.25 USD/BBL for 2023, depending on the region. Prices sit relatively high today at over $100/BBL.

The industry is seeing a consistent increase in demand, with passenger and cargo traffic rising since COVID lockdowns lifted, now within 3% of pre-COVID levels (see chart below).

Rising refined product demand is being led by jet fuel in Asia this year originally due to China’s delayed COVID reopening.

Demand growth will slow in 2025. After two years of strong growth, the initial pump of mainland China’s reopening and consequent jet fuel rebound will subside. Refined products demand to grow 0.6 million b/d in 2025 versus 2.0 million b/d (2023) and 1.1 million b/d (2024).

Peak demand for jet fuel will likely come later in the long-term vs. other refined products due to the energy density requirements of flying.

Global refining capacity for jet fuel is set to increase, from the likes of Oman’s Duqm (230 kbd total refined product capacity), Iraq’s Karbala (140 kbd), Kuwait’s Al Zour (615 kbd), Nigeria’s Dangote (650 kbd) and Texas’ Beaumont expansion (250 kbd).

Commercial jet fuel inventories are at 105 million barrels (+4 million YoY) – in ARA they sit in the bottom half of their historical range, U.S. stocks in the top half of their 5-year range and in Japan slightly above their historical average.

Aviation Industry Challenges

Forecasting aviation fuel demand: Pent-up travel demand post-COVID, supported by monetary stimulus, has helped overcome inflationary cost pressures – but this is expected to be temporary as macroeconomic headwinds start to bite consumer spending. This will result in softening air travel demand growth.

→ Industry Challenge: accurately forecast air traffic and jet fuel demand for improved fuel supply planning by location, to help airlines and fuel suppliers manage supply availability, manage supply crises and design contingency planning.

Industry costs related to sustainability and the energy transition are likely to grow due to regulatory interventions and policy mandates.

→ Industry Challenge: there is a lack of certainty and clarity around current policy, upcoming changes and how these will affect fuel markets and region-specific operational requirements – especially recently in the likes of Europe with strong mandates that are purposefully kept flexible and open to interpretation, thus leading to confusion between market players.

Jet fuel pricing: jet fuel is typically 25% of an airline’s operating costs and this has increased in the past year towards 30% in line with fuel prices. Every $1 increase in jet fuel prices results in a $2 billion cost to the industry. Therefore elevated oil prices squeezes airline margins further. Additionally, airlines need to understand where to tanker¹ fuel from during crises and forecast shortages to mitigate unplanned costs and flight disruptions.

→ Industry Challenge: have daily visibility on jet fuel prices by region and forecasts to use in cashflow models, quarterly budgeting and route planning.

Jet fuel supply security: Understand which refineries have outages to better plan for jet supply disruptions both immediately and seasonally.

→ Industry Challenge: have near real-time visibility on refinery disruptions and their subsequent impacts on supply availability.

Identify arbitrage trading opportunities: the more sophisticated traders ingest data from multiple energy market data providers (Bloomberg, S&P Global, WoodMackenzie, Kpler…) → pinpoint discrepancies between the fundamentals to identify potential dislocations → gauge any geographic or time arbitrage opportunities → build a model or trading strategy to optimize for this → back-test this model/strategy on historical data → decide whether to action on it under current market conditions. This applies to many commodities.

→ Industry Challenge: have sufficiently up-to-date data across geographies to benchmark and model fundamentals.

Skill/labour shortages for airlines and aviation infrastructure means rising costs and operational impacts. Low unemployment rates makes it harder to acquire and retain talent in the airline industry as the labour supply is tight – leading to staff shortages and wage inflation – contributing to higher operational costs.

→ Industry Challenge: have an independent assessment for inflationary price increases and commentary on labour market changes.

Cost premiums of SAF vs. jet fuel: SAF prices are at least double those of jet fuel, therefore while the technology scales up, it needs to become more economically viable.

→ Industry Challenge: acquire visibility into SAF prices and production developments, together with the ability to track the spread vs. traditional jet/kero will become increasingly important as demand and policy gradually shift.

Industry Talking Points

Macro & Demand

GDP is growing at a faster pace in emerging economies (4%) vs. advanced economies (1.5%) according the IMF. The outlook is positive for every region in 2024, but subdued. GDP growth is strongly correlated with growth in air travel.

USD trade-weighted exchange rate has been rising since 2012 vs. UK, Eurozone and most other regions – although it is down from its 2022 peak.

Labour markets remain robust, supporting demand while inflation (and potentially interest rates) have likely peaked. Markets tend to factor in interest rate cuts in their price forecasts looking out at 12 – 18 month time horizons.

Jet fuel – crude spreads are elevated together with relatively high oil/jet prices.

Total air passenger traffic is recovering, now within 3% of 2019 levels. Domestic air travel already recovered by April ’23, international RPKs² (Revenue Passenger Kilometers) still lag together with cargo.

Cargo traffic is facing a slightly more pessimistic growth sentiment in the industry; e-commerce has caused a (positive to demand) structural change to air cargo post-COVID. A continuation of this will depend on disposable incomes.

Supply

Supply availability: There are significant challenges in acquiring jet fuel supply in many regions, especially Central Europe, USA, West Africa (Nigeria) and South Africa.

Tankering¹ and fuel stops are a major stress factor for airline operations, leading to higher operational costs and faster aircraft depreciation due to wear and tear.

Supply issues from European refinery closures and Russian sanctions means Europe is more reliant on imported fuels from further away destinations → elongated supply chains with an increased number of vulnerabilities (e.g. Suez canal congestion, Rhine water levels for barge transportations, truck driver shortages in various countries, French strikes resulting in oil tankers avoiding French ports…).

Supply chain security: climate protesters or terrorists sabotaging infrastructure. E.g. cases have been reported recently at a Scottish refinery, with cyber-attacks at German energy infrastructure and at pipelines in both Nigeria and Norway.

Europe: Arab Gulf and India largest supply sources of jet fuel, although post-COVID the Far East has stepped up to compensate for the lack of Russian imports.

Africa: long supply lead times, especially in ports like Beira in Mozambique where demurrage can be as much as 75 days at a cost of $30,000 - $50,000/day. More storage is being built to combat this, but this is far from a full solution. South Africa’s rail system is too unreliable with frequent cable thefts, derailments and breakdowns. Dangote in Nigeria should eventually alleviate large supply bottlenecks in West Africa.

Energy Transition

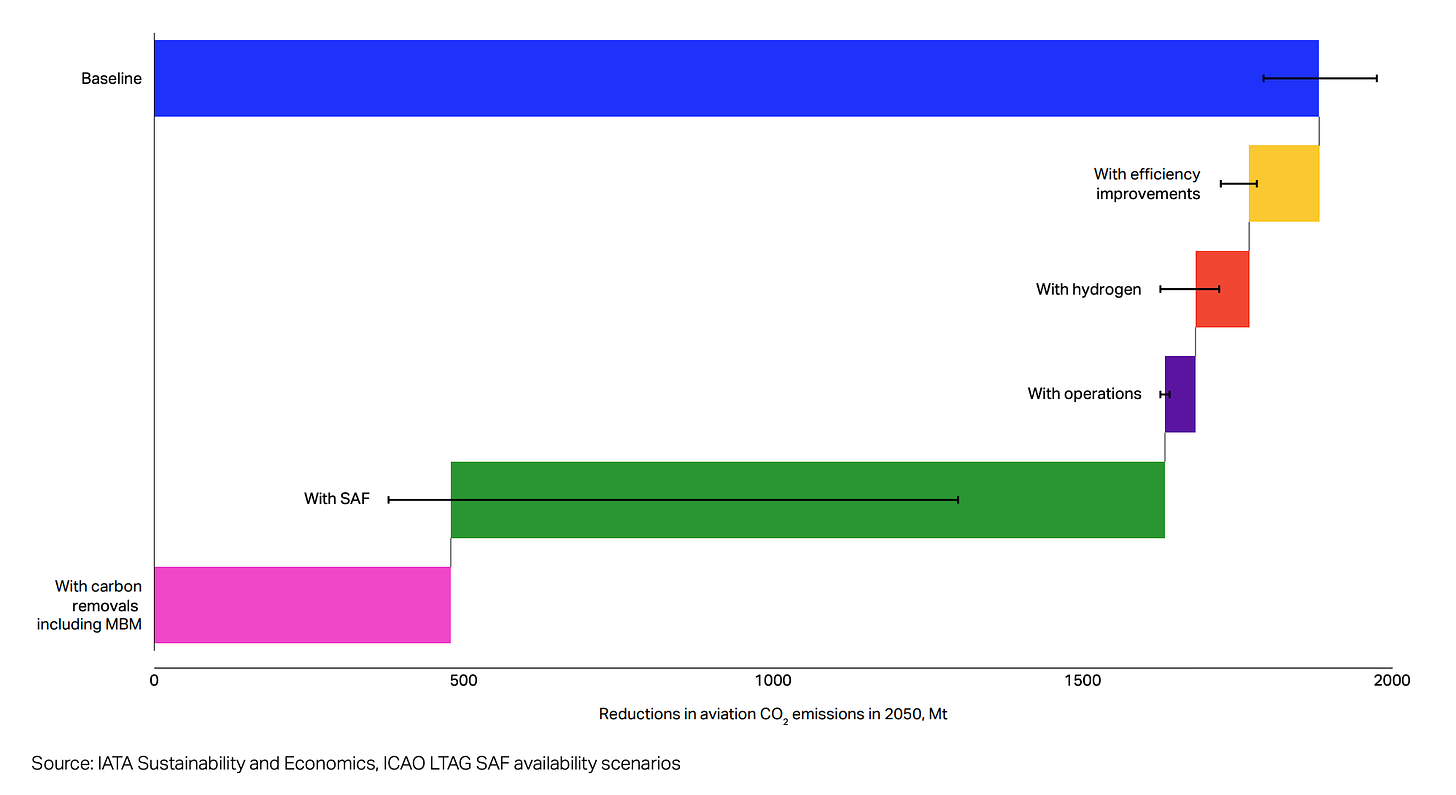

In 2021, the aviation industry made the big decision to commit to reaching net zero CO2 emissions by 2050. However, aviation is one of the most difficult industries to decarbonise as jet fuel has a very high energy density (43 megajoules/kg) and is lighter and more transportable than e.g. giant batteries. Every 1kg of jet fuel burned produces 3kg of CO2. Some mechanisms to reduce emissions (source: IATA):

Reduce in-flight energy use through incremental improvements in aircraft energy efficiency – forecasted to contribute to 7.5% fewer emissions by 2050.

Change the fuel to SAF (65% fewer emissions) and hydrogen (4.8% fewer emissions) at scale by 2050. Dubai-based airline Emirates just piloted its first SAF-fuelled flight this week.

Improving all currently visible operational efficiencies (e.g. turning off engines when stationary) would mean 2.6% fewer emissions.

Recapture emitted CO2, CCUS.

The solid bar indicates IATA’s central case and the black lines indicate maximum and minimum reductions based on their modelled scenarios

Definitions

¹ Tankering: The practice of fuel tankering is when an aircraft deliberately carries excess fuel in order to reduce or eliminate refuelling at its destination. When a destination is known to be selling aircraft fuel at a higher cost than the airport of origin, airlines will sometimes carry extra fuel on board to minimize the amount they spend when they arrive. Alternatively, this may be done if there is not enough fuel at a destination airport.

² RPKs: Revenue Passenger Kilometers is an airline industry metric that shows the number of kilometers traveled by paying passengers. It is calculated as the number of revenue passengers multiplied by the total distance traveled. Since it measures the actual demand for air transport, it is often referred to as airline “traffic.”